Cross-Border Transaction Tracing: How UK Casino Apps Flag Suspicious Patterns in Real Time for Regulatory Oversight

UK casino apps process thousands of cross-border payments daily, and operators rely on automated systems that scan each transfer for indicators of money laundering or other financial crimes. These platforms pull data from payment processors, bank ledgers, and user profiles, then apply rule-based filters alongside machine learning models to spot velocity spikes, mismatched IP locations, and unusual currency flows within seconds of initiation.

Core Detection Mechanisms in Mobile Platforms

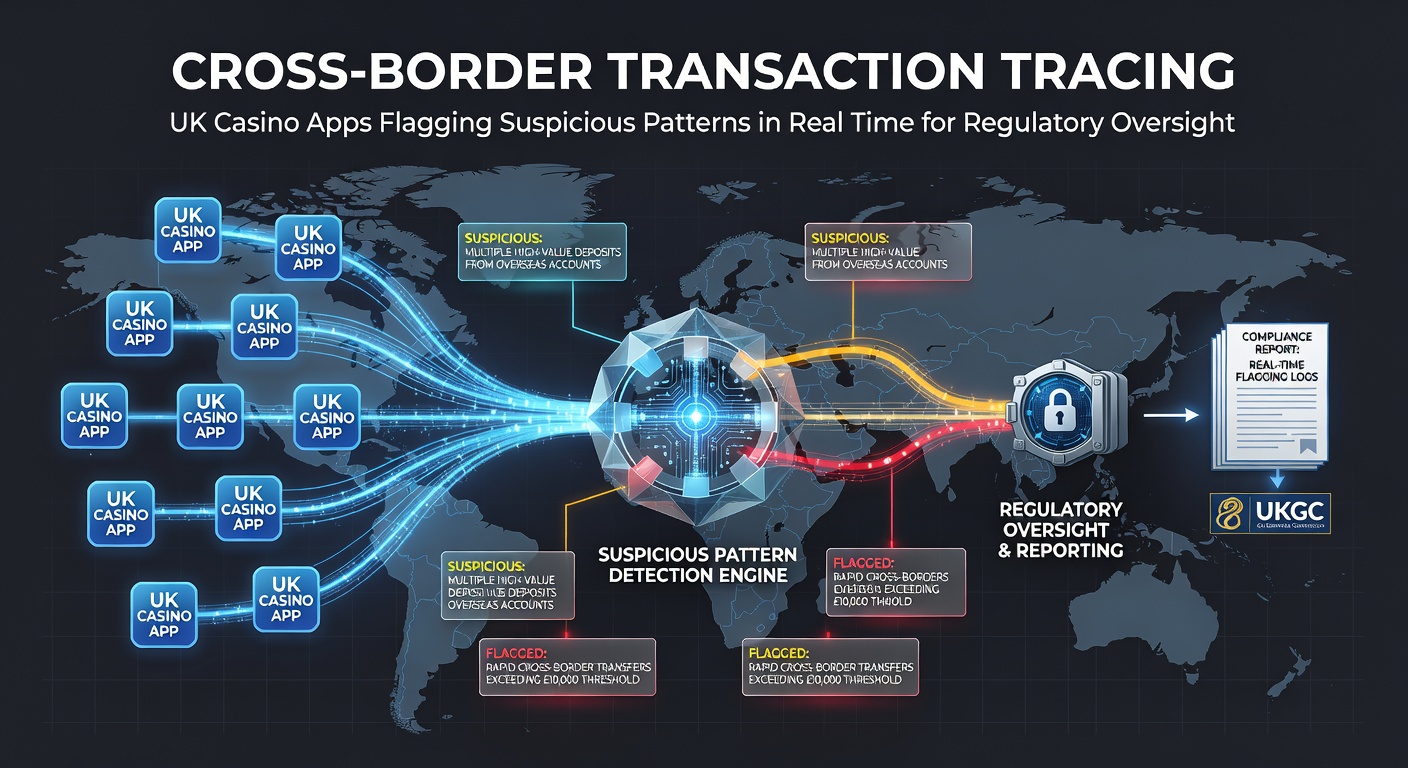

Transaction tracing begins at the deposit stage when an app records the originating country, payment rail, and wallet address. Algorithms compare the new entry against historical patterns for that account, while cross-referencing global watch lists maintained by financial intelligence units. If a transfer originates from a high-risk jurisdiction yet claims a UK billing address, the system raises an alert and may require additional verification before funds clear.

Real-time scoring engines assign risk values based on multiple variables at once. A single large deposit from an unfamiliar European bank might score low, yet the same amount arriving minutes after a withdrawal to an Asian crypto exchange can push the combined score over internal thresholds. Staff receive dashboards that highlight these linked events rather than isolated transactions.

International Data Sharing and Reporting Timelines

Operators feed flagged cases into secure portals shared with overseas counterparts, allowing rapid queries across borders. When patterns suggest layering through multiple countries, the data travels to bodies such as the Financial Action Task Force network or national units like AUSTRAC in Australia. These exchanges follow standardized formats that emerged from mutual evaluation rounds conducted in recent years.

By June 2026 several platforms had integrated API connections that deliver preliminary reports to regulators within four hours of a suspicious trigger, shortening the previous twenty-four-hour window. The shift stems from updated technical standards issued by regional supervisors who coordinate with UK entities on cross-border flows.

Pattern Recognition Examples Observed in Practice

One documented scenario involved repeated micro-deposits from a single Eastern European card that funded accounts later used to place low-risk bets before immediate withdrawals to a different continent. The velocity and geographic mismatch triggered sequential alerts that compliance teams reviewed in under fifteen minutes. Another case revealed a cluster of accounts sharing device fingerprints yet routing funds through three separate currencies in quick succession, prompting a coordinated freeze across multiple operators.

Researchers at the University of Toronto examined similar datasets from North American and European operators and found that combining device telemetry with payment metadata reduced false positives by roughly thirty percent compared with payment data alone. Their published analysis highlights how graph-based algorithms map relationships between accounts that traditional rules overlook.

Regulatory Expectations Around Audit Trails

Supervisors require that every automated decision carries an immutable log showing the exact rules or model outputs that generated an alert. These logs must remain accessible for at least five years and support reconstruction of the decision path during external reviews. Periodic testing of detection thresholds occurs through simulated transaction batches supplied by regulators themselves.

Third-party auditors sample live data feeds quarterly to verify that cross-border indicators receive consistent treatment across different app versions. When gaps appear, operators must adjust model weights and document the changes before the next reporting cycle.

Challenges With Emerging Payment Methods

Crypto and e-wallet rails introduce additional complexity because wallet addresses can route through mixers or privacy coins. Apps now embed blockchain analytics services that tag high-risk addresses in real time, feeding those tags directly into the same scoring engine used for fiat transactions. Staff training programs emphasize recognizing obfuscation techniques that have surfaced in enforcement actions reported by Canadian and Singaporean authorities.

Conclusion

Cross-border transaction tracing in UK casino apps rests on layered detection that combines payment metadata, device signals, and international data exchange. Automated systems generate alerts within seconds while maintaining detailed records that satisfy oversight requirements from multiple jurisdictions. Continued refinement of these tools depends on cooperation between operators, technology vendors, and financial intelligence units operating beyond UK borders.